WHAT IS THE POLITICAL SUBDIVISION WORKERS’ COMPENSATION ALLIANCE AND HOW DOES IT RANK AT SERVING OUR MEMBERS? Operational Excellence in Acti...

3 min read

You’ve probably heard it before... not all coverage is the same. Or, perhaps you’ve heard the phrase, “What the BIG print giveth, the little print taketh away.” If you haven’t, don’t feel bad, it’s a joke only insurance nerds would appreciate 😊. Nevertheless, even though two coverage documents from different providers may have the same name, the coverage provided may very well be like apples and oranges. This is certainly the case when comparing any type of “claims-made” coverage to “occurrence” based coverage.

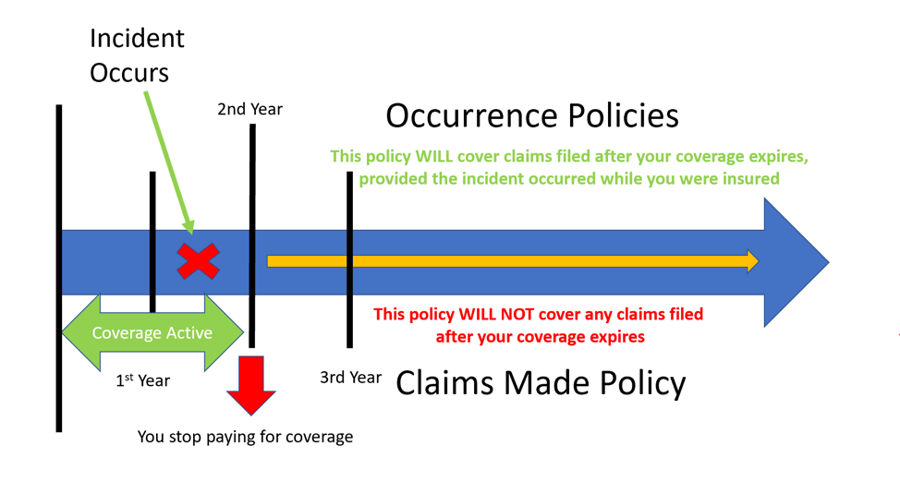

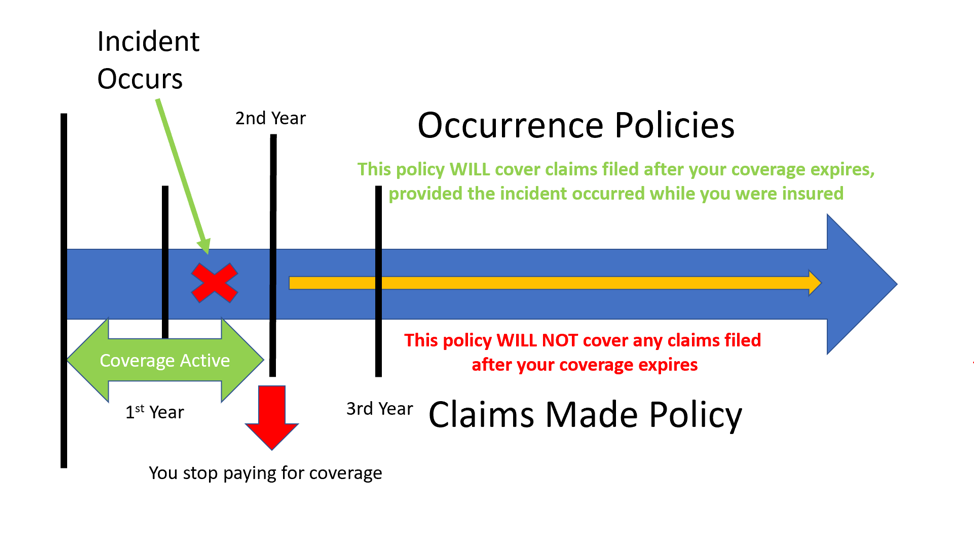

Consider the following scenario: The Human Resources Director receives a lawsuit alleging discrimination. The lawsuit alleges the discrimination took place 2 years ago. At the time the city had coverages with ABC insurance, and that policy was claims-made. Their current policy is occurrence based with no retroactive date for prior incidents (sorry for the insurance speak, but stay with it, this is an important point that we’ll try to make clear). The HR director contacts the current provider only to find out there’s no coverage since the incident occurred prior to the inception of that policy. No problem, until a call is then made to the prior insurer only to learn that there is no coverage through that either, because coverage was terminated two years ago. The HR Director is not having a good day. The worst time to find that there is no coverage is after a claim is submitted. Let’s explore how to remedy this problem. In the example above, the City was left without coverage after moving liability coverage from one provider to another. Below is a timeline of the events with an explanation of the difference in claims-made versus occurrence type policies.

Claims-made coverage simply means the claim must be made during the policy period, i.e.the coverage is triggered when a claim is made during the policy period, regardless of when the wrongful act that gave rise to the claim took place. (Two exceptions might apply: an extended period to report claims is purchased from the claims-made carrier upon termination; or the new carrier provides a retroactive period for reporting of claims for prior incidents. In such instances, the wrongful act that gave rise to the claim must have taken place during the extended reporting period or within the retroactive period.)

Most professional, errors and omissions (E&O), directors and officers (D&O), and employment practices liability insurance (EPLI) is written on a claims-made basis.

Coverage is triggered under occurrence-based policy so long as the claim occurs during the policy period, regardless of when it is reported and even if coverage has been moved to a different insurer when the claim is actually filed. Occurrence coverage is often deemed superior since professional liability claims are often made long after the incident giving rise to the claim occurs. The advantage of an occurrence-based policy is its permanence. The period of time you are insured under an occurrence policy is protected forever by the policy you had in place when the incident occurred.

Should you have a claims-made policy and change carriers, an extended reporting period, mentioned earlier and known as “tail coverage”, is needed in order to provide protection for incidents that have occurred, but no claim has been filed. Tail coverage is usually available, but at an additional cost, which can be significant.In addition, most tail provisions have limited reporting provisions, typically 1, 3, 5 or possibly 10 years. Nevertheless, it is often advisable to purchase tail coverage when switching from a claims-made policy. Please note, coverage through the Risk Pool is on an occurrence basis and retroactive coverage is provided for up to 5 years at no additional cost. Tail coverage can be quite costly and should be factored in when comparing the cost of coverage.

The obvious question becomes, “why would anyone purchase a claims-made policy if occurrence-based policies are superior?” There are a few reasons. A claims-made policy may be all that is available. As an example, employment practices liability, may only be available under the claims-made form from a private carrier. Other coverages may be available on either type of form, but the occurrence version is likely more expensive given the breadth of coverage.

In summary, pay close attention to the type of coverage form (occurrence or claims-made) when considering liability coverage options. Additionally, the costs, both on the front end and back end, should be considered. When switching carriers additional retroactive or tail coverage may be advisable, depending upon the coverage form. Also consider tail coverage may be a future cost for claims-made coverage.

Please contact the Risk Pool’s member services department for more information on this or any other coverage need.